Momenta's Take #15

The semiconductor industry is seeing a wave of significant consolidation fueled by strong gains in the equity markets. Over the past two months two of the three largest acquisitions ever have been announced: AMD communicated that it plans to purchase Xilinx for $35 billion, just weeks after Nvidia agreed to acquire Arm from SoftBank for approximately $40 billion. The two deals are similarly sized to Avago’s $37 billion purchase of Broadcom in 2015.

M&A activity in tech has been lumpy this year but are showing dramatic signs of acceleration. For the first 6 months of the year, merger activity largely paused because of the uncertainties around the pandemic and meltdowns in equity markets in March. Typically, a weak stock market will depress sentiment of buyers for a couple of reasons:

- Extrapolating that market valuations are a leading indicator of fundamentals; weak share prices suggest uncertainty in the business outlook and

- Public companies that wish to use their equity as currency for acquisitions have less to work with when stock prices are low.

The exception is of course, that buyers with strong balance sheets can be opportunistic and make cash acquisitions, and investors in publicly traded equities always seek to “buy low and sell high”. This approach certainly makes sense for investors, but not necessary for strategic acquirers who are looking for 2+2=5 synergies from deals. The other caveat in a period of depressed share prices is that management teams and boards are less willing to approve a sale at a price less than they think the company is worth, and when there’s a reset of stock prices downward across the board, it’s often better to ride it out until valuations improve.

We saw this dynamic play out in a big way in the first half of 2020. According to Merger Markets, global M&A was down significantly for the first two quarters of the year, but in the 3rd Quarter, large deals (over $5 billion in disclosed value) skyrocketed 256% quarter over quarter with 32 transactions totaling $451.3 billion. Tech, Media and Telecom (TMT) have seen a robust rebound. With the pandemic accelerating adoption and rollout of online and remote services, this drove aggressive investment making TMT the most active sector in M&A with 760 deals totaling $301.2 billion (not including the possible divestiture of TikTok by ByteDance, which could reach $60 billion).

The renewed interest in deal making following a pause for the pandemic is evidenced in a recent survey of over 1,000 decision makers by Deloitte. When asked “Since March 2020, how has deal making been impacted in terms of your company’s pursuit of new deals?” over 60% responded that appetite for M&A had increased, while only 16% indicated they are less focused on new deals.

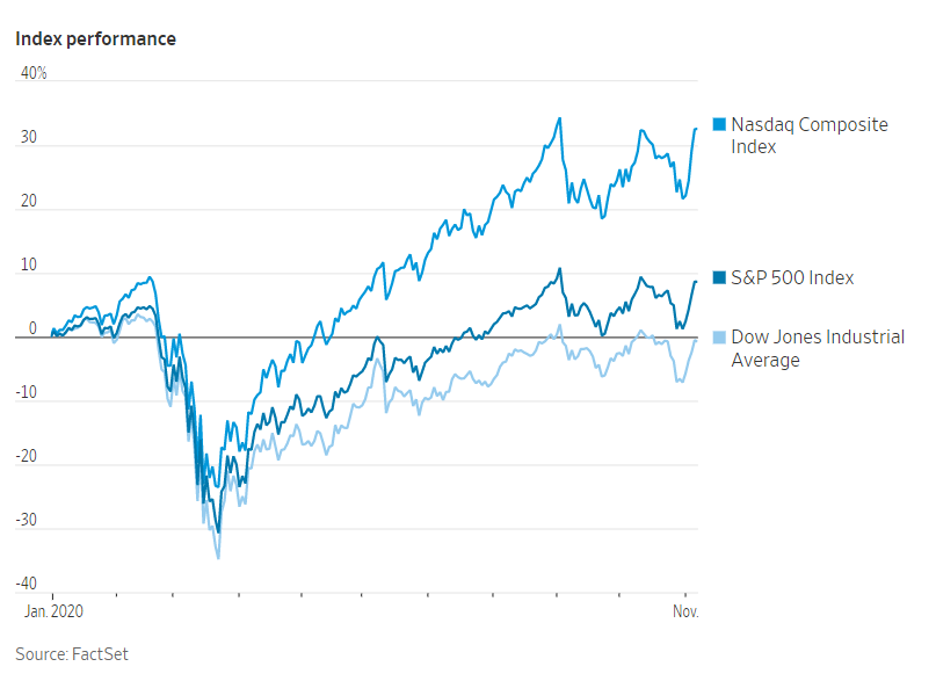

The rally in the stock market following the U.S. election has pushed indexes into positive territory for 2020, despite the lingering challenges of the pandemic. The tech-heavy NASDAQ is up 33% and the S&P 500 up 9%, versus a 1% decline in the Dow Jones Industrial Average. Additionally, corporate profits have been resilient, boosting confidence in strong economic fundamentals as the world economy recovers from the COVID-19 shutdowns.

Following the results of the U.S. elections it appears that challenger Joe Biden defeated the incumbent Donald Trump, with the Republicans on track to hold the Senate with a Democrat-held House. The markets like divided government, as it means that neither side is likely to implement any dramatic changes to the current business environment.

Combine higher stock prices with improving corporate sentiment regarding M&A and you get the conditions for accelerating deal activity – and tech is at “ground zero”. Look for 2021 to shape up as one of the busiest years for deals yet!

Unlock the Power of Digital - Momenta encompasses leading Strategic Advisory, Talent, and Ventures practices for Digital Industry. Connect with us to find out more about our three practices and how we deliver digital value.